Contacto

Contacto Cómo comprar

Cómo comprarEntrega

Guía de compras

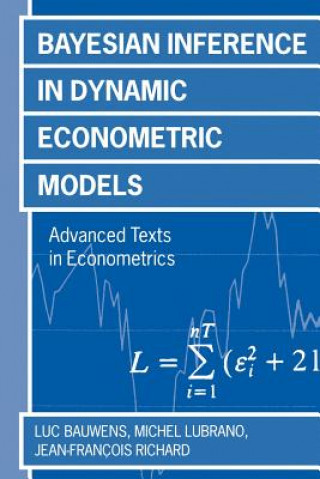

Bayesian Inference in Dynamic Econometric Models

Inglés

Inglés

229 b

229 b

Política de devolución de 30 días

Clientes que también han comprado

/

/

Tapa dura

Tapa dura

28.89

€

28.89

€

/

Tapa blanda

39.39

€

/

Tapa blanda

39.39

€

This book contains an up-to-date coverage of the last twenty years advances in Bayesian inference in econometrics, with an emphasis on dynamic models. It shows how to treat Bayesian inference in non linear models, by integrating the useful developments of numerical integration techniques based on simulations (such as Markov Chain Monte Carlo methods), and the long available analytical results of Bayesian inference for linear regression models. It thus covers a broad range of rather recent models for economic time series, such as non linear models, autoregressive conditional heteroskedastic regressions, and cointegrated vector autoregressive models. It contains also an extensive chapter on unit root inference from the Bayesian viewpoint. Several examples illustrate the methods.

Sobre el libro

Inglés

Categorías

Regale este libro hoy

Es fácil

1 Añadir al carrito y elegir Entregar como regalo en el checkout 2 Le enviaremos un vale 3 El libro llegará a la dirección del destinatarioTambién puede interesarle

/

Tapa blanda

14.29

€

/

Tapa blanda

14.29

€

/

Tapa blanda

31.49

€

/

Tapa blanda

31.49

€

/

Tapa dura

106.79

€

/

Tapa dura

106.79

€

/

Tapa dura

24.29

€

/

Tapa dura

24.29

€

/

Tapa blanda

19.09

€

/

Tapa blanda

19.09

€

/

Tapa dura

119.29

€

/

Tapa dura

119.29

€

/

Tapa blanda

12.69

€

/

Tapa blanda

12.69

€

¡Hola! Soy Libroamiko, tu asesor de libros.

¿Cómo puedo ayudarte?