Contacto

Contacto Cómo comprar

Cómo comprarEntrega

Guía de compras

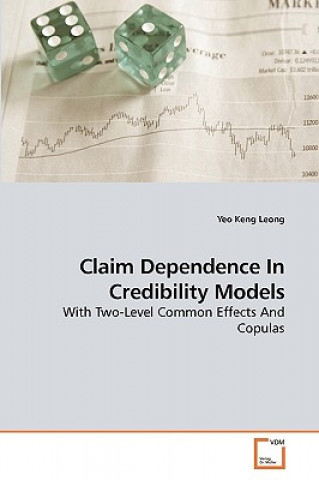

Claim Dependence In Credibility Models

Inglés

Inglés

179 b

179 b

Hasta 30 días para devoluciones

Clientes que también han comprado

/

/

Tapa blanda

Tapa blanda

17.29

€

17.29

€

/

Tapa blanda

27.29

€

/

Tapa blanda

27.29

€

/

Tapa blanda

33.79

€

/

Tapa blanda

33.79

€

Existing credibility models usually allow for one source of claim dependence only, that across time, which may be inadequate and insufficient. In this dissertation, we develop a two-level common effects model, based loosely on the Bayesian model. This model allows for two possible sources of dependence, that across time for the same individual risk and that between risks. Our results take on the intuitive form of a weighted average between the individual risk s claims experience, the group s claims experience and the prior mean. We also consider the use of copulas to model the dependence across time. We develop the construction with several well-known families of copulas and are able to derive explicit formulae for their respective conditional expectations. Whilst some recent work has been done on constructing credibility models with copulas, explicit formulae for the conditional expectations have rarely been made available. This work will be useful for practitioners and researchers alike, in furthering our collective understanding of dependence between insurance risks and its potential impact on insurance prices.

Sobre el libro

Inglés

Categorías

Regale este libro hoy

Es fácil

1 Añadir al carrito y elegir Entregar como regalo en el checkout 2 Le enviaremos un vale 3 El libro llegará a la dirección del destinatarioTambién puede interesarle

/

Tapa blanda

37.39

€

/

Tapa blanda

37.39

€

/

Tapa dura

42.59

€

/

Tapa dura

42.59

€

¡Hola! Soy Libroamiko, tu asesor de libros.

¿Cómo puedo ayudarte?