Contacto

Contacto Cómo comprar

Cómo comprarEntrega

Guía de compras

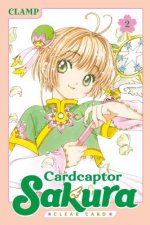

Convolution Copula Econometrics

Inglés

Inglés

161 b

161 b

Política de devolución de 30 días

Clientes que también han comprado

/

/

Tapa dura

Tapa dura

124.19

€

124.19

€

/

Tapa blanda

112.79

€

/

Tapa blanda

112.79

€

This book presents a novel approach to time series econometrics, which studies the behavior of nonlinear stochastic processes. This approach allows for an arbitrary dependence structure in the increments and provides a generalization with respect to the standard linear independent increments assumption of classical time series models. The book offers a solution to the problem of a general semiparametric approach, which is given by a concept called C-convolution (convolution of dependent variables), and the corresponding theory of convolution-based copulas. Intended for econometrics and statistics scholars with a special interest in time series analysis and copula functions (or other nonparametric approaches), the book is also useful for doctoral students with a basic knowledge of copula functions wanting to learn about the latest research developments in the field.

Sobre el libro

Inglés

Regale este libro hoy

Es fácil

1 Añadir al carrito y elegir Entregar como regalo en el checkout 2 Le enviaremos un vale 3 El libro llegará a la dirección del destinatarioTambién puede interesarle

/

Tapa blanda

48.79

€

/

Tapa blanda

48.79

€