Contacto

Contacto Cómo comprar

Cómo comprarEntrega

Guía de compras

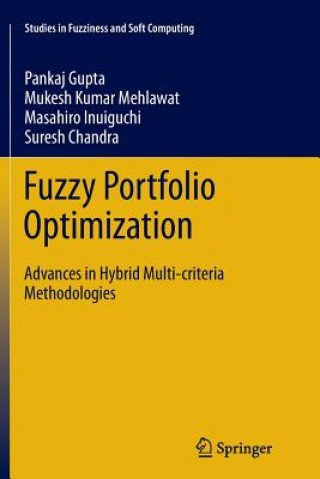

Fuzzy Portfolio Optimization

Advances in Hybrid Multi-criteria Methodologies

Inglés

Inglés

441 b

441 b

Política de devolución de 30 días

Clientes que también han comprado

/

/

Tapa blanda

Tapa blanda

30.09

€

30.09

€

/

Tapa dura

71.99

€

/

Tapa dura

71.99

€

/

Tapa blanda

20.59

€

/

Tapa blanda

20.59

€

This monograph presents a comprehensive study of portfolio optimization, an important area of quantitative finance. Considering that the information available in financial markets is incomplete and that the markets are affected by vagueness and ambiguity, the monograph deals with fuzzy portfolio optimization models. At first, the book makes the reader familiar with basic concepts, including the classical mean-variance portfolio analysis. Then, it introduces advanced optimization techniques and applies them for the development of various multi-criteria portfolio optimization models in an uncertain environment. The models are developed considering both the financial and non-financial criteria of investment decision making, and the inputs from the investment experts. The utility of these models in practice is then demonstrated using numerical illustrations based on real-world data, which were collected from one of the premier stock exchanges in India. The book addresses both academics and professionals pursuing advanced research and/or engaged in practical issues in the rapidly evolving field of portfolio optimization.

Sobre el libro

Inglés

Regale este libro hoy

Es fácil

1 Añadir al carrito y elegir Entregar como regalo en el checkout 2 Le enviaremos un vale 3 El libro llegará a la dirección del destinatarioTambién puede interesarle

/

Tapa dura

92.79

€

/

Tapa dura

92.79

€

/

Tapa blanda

11.19

€

/

Tapa blanda

11.19

€

/

Tapa dura

219.69

€

/

Tapa dura

219.69

€

¡Hola! Soy Libroamiko, tu asesor de libros.

¿Cómo puedo ayudarte?