Envío gratis a partir de 69,99 euros.

Entre a formar parte de una comunidad de amantes de los libros del mundo entero y acceda a un sinfín de ventajas.

Crear una cuenta gratis

Envío gratuito con Zásilkovna para compras superiores a 59.99 €

Mensajería SEUR 4.99 €

Mensajería GLS 7.99 €

Mensajería Correos 5.49 €

Mensajería DHL 5.49 €

Punto SEUR 3.99 €

Contacto

Contacto Cómo comprar

Cómo comprar

Ayuda

Entrega

Mensajería SEUR 4.99 €

Mensajería GLS 7.99 €

Mensajería Correos 5.49 €

Mensajería DHL 5.49 €

Punto SEUR 3.99 €

Envío gratuito con Zásilkovna para compras superiores a 59.99 €

Guía de compras

Mi cuenta

▸

Vacío :-(

0

Envío gratis a partir de 69,99 euros.

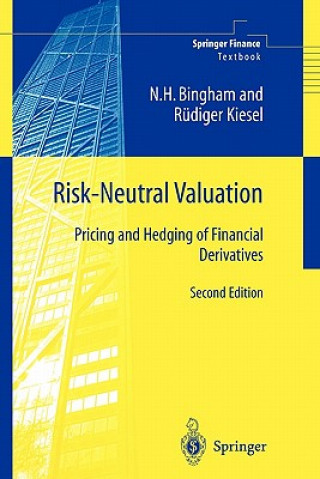

Risk-Neutral Valuation

Pricing and Hedging of Financial Derivatives

Idioma

Inglés

Inglés

Inglés

Libro

Tapa blanda

This second edition - completely up to date with new exercises - provides a comprehensive and self-c...

Descripción completa

Código Libristo: 01434764

?

176 b

176 b

176 b

71.99

€

Almacenamiento externo

Envío en 5-8 días

Hasta 30 días para devoluciones

Clientes que también han comprado

/

/

Tapa blanda

Tapa blanda

15.39

€

15.39

€

/

Tapa blanda

49.19

€

/

Tapa blanda

49.19

€

/

Tapa blanda

15.09

€

/

Tapa blanda

15.09

€

/

Hoja

14.19

€

/

Hoja

14.19

€

This second edition - completely up to date with new exercises - provides a comprehensive and self-contained treatment of the probabilistic theory behind the risk-neutral valuation principle and its application to the pricing and hedging of financial derivatives. On the probabilistic side, both discrete- and continuous-time stochastic processes are treated, with special emphasis on martingale theory, stochastic integration and change-of-measure techniques. Based on firm probabilistic foundations, general properties of discrete- and continuous-time financial market models are discussed.

Actriz

&

Políglota

EWA KASP

para

Visualizar el vídeo

Libristo tiene la oferta más extensa de literatura en idiomas extranjeros. Por eso compran aquí sus libros.

Sobre el libro

Nombre y apellidos

Risk-Neutral Valuation

Idioma

Inglés

Inglés

Encuadernación

Libro - Tapa blanda

Fecha de publicación

2010

Número de páginas

438

EAN

9781849968737

ISBN

184996873X

Código Libristo

01434764

Editores

Springer London Ltd

Peso

682

Dimensiones

158 x 233 x 24

Regale este libro hoy

Es fácil

1 Añadir al carrito y elegir Entregar como regalo en el checkout 2 Le enviaremos un vale 3 El libro llegará a la dirección del destinatarioTambién puede interesarle

Asesor de libros Libroamiko

Al usar este chat, te estás comunicando con inteligencia artificial generativa. Al usarlo, también aceptas el tratamiento de datos personales.

¡Hola! Soy Libroamiko, tu asesor de libros.

¿Cómo puedo ayudarte?

Hola, soy Libroamiko, ¿puedo ayudarte?